BlackBerry в России

Управление мобильностью предприятия (EMM), в перспективе, как правило, рассматривается как «один-размер-подходит-всем».

В основу закладывается одна из моделей BYOD, COPE или CYOD. Но на самом деле, когда дело доходит до управленческих нужд большинства организаций, кроме самых маленьких предприятий, требуется сочетания сценариев управления, чтобы покрыть потребности мобильности предприятия, которые зависят от географии, нормативных требований, роли, рисков и ряда других факторов.

COPE (Corporate- Owned, Personally Enabled) корпоративное устройство с возможностью частного использования.

CYOD (Choose Your Own Device) покупка сотрудником собственного устройства для работы

BYOD (Bring Your Own Device) использование сотрудником собственного устройства для работы

Различные сценарии

«Понятно, что когда дело доходит до планирования и реализации стратегии мобильности, нет одной политики, которая подойдет всем организациям», заключает недавний отчет исследовательской компании Ovum. «Нет, одного правильного или неправильного способа ведения дел — но есть определенные стратегии и решения, которые могут быть более подходящими в различных сценариях».

В докладе далее говорится, что организации в регулируемых или сильно защищенных средах часто требуют соблюдения стратегии управления мобильными устройствами, известное как Corporate-Owned, Business-Only (COBO) (Корпоративная собственность, только для работы), по крайней мере, для части своей рабочей силы. Ovum цитирует BlackBerry как «создателя и наиболее известного поставщика предлагающего пакет аппаратного и программного обеспечения для развертывания COBO, и остается лидером с точки зрения безопасности и управления устройствами от начала и до конца».

Посмотрим правде в глаза — нарушения случаются, будь то взломы, кражи компьютеров или устройств, или результате случайных утечек или просто случайных неудач. Итоговая стоимость для компаний и государственных учреждений может быть огромной, на сумму в сотни миллионов в случае Target, или 3,5 млн. долл. США в год в среднем, по данным исследования, у IBM.

Опираясь на BES10

EMM платформа BlackBerry, BlackBerry Enterprise Service 10 (BES10), превратилась в последние годы в мульти-платформенное решения для управления и обеспечения безопасности устройств на базе iOS, Android и BlackBerry. BES10 предоставляет клиентам гибкость позволяя применять любую модель политики — от открытого BYOD до Corporate Only, Personally Enabled (COPE), допускающего использование смартфона в личных целях и до полностью контролируемого COBO для сред с высоким уровнем безопасности. На самом деле, правительственные учреждения, компании в регулируемых рынках и любой бизнес, который требует повышенной безопасности и контроля продолжают обращаться к смартфонам BlackBerry 10 и BES10, как единственному варианту корпоративного класса COBO.

Главная характеристика COBO, это опции управления устройством BlackBerry предоставляющие возможность ограничить использование смартфонов только для вычислений и коммуникационной деятельности, связанных с работой. BlackBerry COBO также предоставляет IT-администраторам возможность наложить ограничения на устройство, приложения и управление данными для обеспечения соблюдения этих требований.

Опции COBO для управления мобильностью предприятия предназначены для организаций, которые все чаще сталкиваются с обременительным набором требований соответствия для предотвращения последствий утечки данных. Финансовые услуги, услуги здравоохранения и государственного сектора, в частности, были затронуты законодательством в последние годы, и теперь требуют точного аудита всех электронных транзакций, в том числе, по электронной почты, сообщений и голосовых вызовов.

Решение этих строгих нормативных требований с менее консервативным подходом к управлению мобильностью предприятия, в частности BYOD, трудно — если не невозможно.

Не только в регулируемом секторе

Но дело не только в регулируемом, корпоративном секторе, который требует COBO. Бизнес-подразделения, или даже отдельные руководители, на крупных предприятиях часто требуют ультра-ограничивающий элемент управления COBO, который позволяет защитить компанию от кражи интеллектуальной собственности, утечки данных, от воздействие юридической ответственности за нарушения законов или правил.

Конечно, COBO не для всех. Но откровения органов контролирующих интернет и мобильную связь и случаи промышленного шпионажа также могут способствовать ужесточению мобильной безопасности.

Возможные признаки всплеска более консервативных подходов к управлению мобильностью предприятия можно найти в отчете от мая 2014 года Strategic Analytics, Global Business Smartphone Shipments Forecast: Q1 2014 Update. Хотя личные смартфоны будут прежнему превышать число корпоративных бизнес-смартфонов с перевесом 2-к-1 до 2018 года, темпы роста числа личных телефонов на предприятиях снижаются гораздо более быстрыми темпами, чем корпоративных, и эта тенденция усилится в ближайшие несколько лет, говорится в докладе.

От COBO до BYOD: весь спектр решений

Быстро движущийся и непредсказуемый характер рынка решений управления мобильностью предприятия побудил организации всех размеров стараться избежать долгосрочных EMM инвестиций.

Самый надежный путь к душевному спокойствию, это партнерством с поставщиком мульти-платформенных EMM решений, который может покрыть полный спектр управления мобильностью от COBO до BYOD.

Подписывайтесь на наши новости, и вы всегда будете в курсе самой последней информации о смартфонах BlackBerry:

Payments on Behalf of (POBO) and Collections on Behalf of (COBO)

Banking Circle’s POBO and COBO solutions give Payments businesses and Banks the ability to offer full payment transparency to their customers across 25 currencies.

The POBO and COBO solutions offer visibility on the sender’s details when processing B2B payments, and the ability to collect funds into Virtual IBAN accounts in the underlying customer’s name.

This improves the efficiency and ease of reconciliation of payments across different jurisdictions, which historically would have been received in the name of the payment provider or bank.

By using POBO and COBO, Payments businesses and Banks can send and receive local and cross border payments on behalf of their customers, while keeping full control of the client relationship.

This not only provides clarity and ease of reconciliation when payments are received, but also allows Payments businesses and Banks to comply with Wire Transfer Regulations (WTR).

Key features

Benefits

Virtual IBAN payouts will display:

Set up requirements

| What is required | What you will receive |

|---|---|

| Customer account names and addresses, or customer account numbers if connecting via SWIFT | A list of Virtual IBANs linked to each customer to store within your system |

| A BIC through SWIFT (connected or non-connected*) | A bulk allocation of new Virtual IBANs to allocate to new customers |

| If a DE IBAN is used, as part of regulatory requirements, the UBO (Ultimate Beneficial Owner) must be provided | Connection via API, UI and SWIFT |

*A non-connected BIC if free of charge from SWIFT

Get in touch

If you are an existing client, please contact your Relationship Manager who will be pleased to assist you.

Холодный кошелёк Cobo Vault

В этом посте мы подробно сделает обзор, про холодный кошелёк Cobo Vault.

Содержание

Ключевые моменты:

Что такое холодный кошелёк для криптовалюты и зачем он мне нужен?

Децентрализованный характер криптовалют — их самая важная особенность, но также и один из самых больших рисков. Это означает, что держатели криптовалюты несут ответственность за безопасность своих собственных криптоактивов, и мало что можно сделать, если вы потеряете свои закрытые ключи или кто — то опустошит ваш кошелёк для криптовалюты.

Некоторые пользователи предпочитают делегировать ответственность за безопасное хранение своих закрытых ключей биржам криптовалют, что, как правило, не лучшая идея. Биржи являются чрезвычайно привлекательными целями для хакеров, и есть также ряд других осложнений, которые могут возникнуть из — за плохого управления, некомпетентности или коррумпированных инсайдеров.

Когда дело доходит до кошельков с криптовалютой, есть несколько вариантов. Возможно, самый простой способ сделать это — использовать бумажный кошелёк, который представляет собой буквально лист бумаги, содержащий ваш закрытый ключ и другую важную информацию. Однако бумажные кошельки неудобны, особенно если вы часто совершаете транзакции со своей криптовалютой.

Второй вариант — использовать программный кошелёк на вашем компьютере или мобильном устройстве. Это гораздо более удобное решение, но оно может поставить под угрозу ваши активы, если ваше устройство взломано или заражено вредоносным ПО.

Когда дело доходит до методов хранения криптовалюты, доступных для обычных держателей криптовалюты, аппаратные кошельки являются самым безопасным вариантом.

Холодные кошельки — это устройства, которые хранят ваши закрытые ключи и используют их для подписи криптовалютных транзакций, не раскрывая сами закрытые ключи внешнему миру.

Холодный кошелёк Cobo Vault

Cobo — компания, занимающаяся безопасностью криптовалюты, которая разработала серию аппаратных кошельков для криптовалюты. Кошельки Cobo Vault первого поколения отличались долговечностью и соответствовали самым современным стандартам водонепроницаемости и устойчивости к падениям.

Тем не менее, все функции долговечности привели к высокой цене, и Cobo решила сделать свои кошельки более доступными со вторым поколением Cobo Vault.

Аппаратные кошельки Cobo Vault второго поколения начинаются с 119 долларов с кошельком Cobo Vault Essential. Если вам нужны дополнительные функции, вы можете получить версию Cobo Vault Pro по цене 169 долларов. В этом обзоре мы в первую очередь будем рассматривать версию Pro, но мы рассмотрим различия между двумя вариантами в отдельном разделе.

Прежде чем мы рассмотрим различные функции кошелька Cobo Vault более подробно, давайте кратко рассмотрим основные преимущества и недостатки этих устройств.

Cobo Vault

Cobo Vault минусы

Обзор возможностей Cobo Vault

Теперь давайте рассмотрим наиболее важные аспекты аппаратных кошельков криптовалюты Cobo Vault. Мы рассмотрим поддерживаемые криптовалюты, форм — фактор, уникальные функции и, конечно же, безопасность устройства.

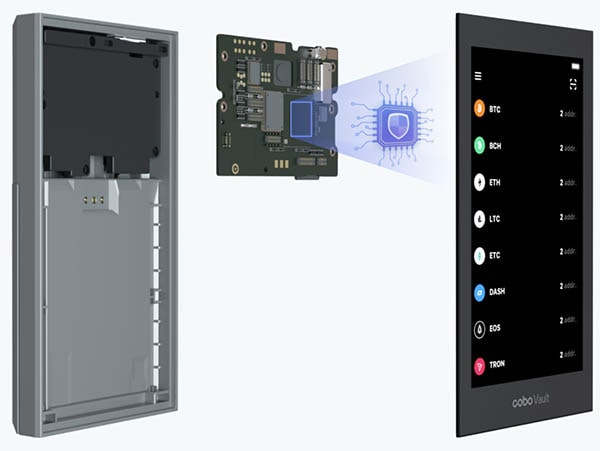

Фактор формы

Кошельки Cobo Vault больше, чем большинство других аппаратных кошельков для криптовалют, особенно по сравнению с предложениями от Ledger и Trezor. Однако устройства оснащены 4 — дюймовым сенсорным экраном, который обеспечивает гораздо более удобное взаимодействие с пользователем по сравнению с конструкциями, основанными на кнопках.

Форм — фактор Cobo Vault сопоставим с меньшим по размеру смартфоном, хотя устройство значительно толще, во многом потому, что Cobo Vault Pro может питаться от батареек AAA. Устройство также оснащено аккумуляторной батареей, что является приятным дополнением для удобства.

Тот факт, что Cobo Vault больше, чем некоторые из его конкурентов, может быть преимуществом или недостатком, в зависимости от пользователя. Больший размер означает, что Cobo Vault сложнее потерять или потерять, но также немного сложнее найти подходящее место для его переноски, например, если вы путешествуете.

Когда вы получите Cobo Vault Pro, в коробке будет:

Особенности безопасности

Само собой разумеется, что безопасность является наиболее важным аспектом любого кошелька с криптовалютой, и команда Cobo предоставила надежный пакет функций безопасности со своими устройствами Cobo Vault.

QR — коды

Вам не нужно подключать устройство Cobo Vault к любому другому устройству, чтобы выполнить транзакцию с криптовалютой. Вместо этого вы используете Cobo Vault для сканирования QR — кода, сгенерированного мобильным приложением Cobo Vault, а затем устройство генерирует QR — код, который вы сканируете с помощью телефона, чтобы фактически начать транзакцию.

Этот метод обеспечивает меньшую поверхность атаки по сравнению с аппаратными кошельками, которые подключаются к другому устройству через USB или Bluetooth. QR-коды, созданные Cobo Vault, можно проверить с помощью любого сканера QR-кодов.

Безопасный элемент

Как и большинство аппаратных кошельков, Cobo Vault имеет защищенный элемент. Проприетарный элемент безопасности, используемый Cobo Vault, имеет сертификат безопасности EAL 5+.

Элемент безопасности отвечает за генерацию случайных чисел, получение пар закрытого и открытого ключей и подписание транзакций. Прошивка безопасного элемента Cobo Vault имеет открытый исходный код, что является долгожданным дополнением. Код доступен на странице проекта Github.

Сканер отпечатков пальцев и механизм самоуничтожения

Эти две функции ограничены Cobo Vault Pro и отсутствуют в версии Essential.

Сканер отпечатков пальцев Cobo, который позволяет вам разблокировать устройство и подписать транзакцию дискретно, без того, чтобы экран показывал ваш пароль окружающим. Эта функция особенно полезна, если вы планируете использовать устройство в людных местах.

Механизм самоуничтожения, с другой стороны, активируется, когда устройство обнаруживает, что кто — то пытается вмешаться в его работу. Как только Cobo Vault Pro обнаруживает, что кто — то пытается разобрать устройство, он мгновенно удаляет всю конфиденциальную информацию, хранящуюся на устройстве.

Механизм самоуничтожения — это линия защиты от атак по сторонним каналам.

Поддерживаемые криптовалюты

Cobo Vault поддерживает 13 различных криптоактивов, а также все токены на основе Ethereum, EOS и TRON. Вот список активов, которые можно хранить в Cobo Vault:

Хотя этот выбор криптовалют надёжен и содержит многие из ведущих криптовалют, он отстает от ключевых конкурентов

Расширение списка поддерживаемых криптовалют — одна из вещей, которые покупатели определенно хотели бы видеть от Cobo, и это также сделало бы устройство более желанным для более широкой аудитории энтузиастов криптовалюты. По заявлению компании, они работают над добавлением поддержки дополнительных монет и токенов.

Cobo Vault Pro против Cobo Vault Essential

Между версией Pro и основной версией Cobo Vault есть 3 основных различия. В версии Essential отсутствует аккумуляторная батарея, а также рассмотренный ранее датчик отпечатков пальцев и механизм самоуничтожения.

Если вам нужны эти 3 функции, Cobo Vault Pro будет стоить вам 149 долларов. В противном случае вам следует купить Cobo Vault Essential, стоимость которого составляет 119 долларов.

По словам разработчиков кошелька Cobo, версия Essential нацелена на долгосрочных пользователей HODL, а версия Pro нацелена на пользователей, которые чаще совершают транзакции со своими криптовалютами и ценят использование своего кошелька на ходу.

Конкуренты Cobo Vault

В настоящее время энтузиасты криптовалюты могут выбирать из множества производителей холодных кошельков:

Вердикт обзора холодного кошелька Cobo Vault

Аппаратные кошельки для криптовалюты Cobo Vault Pro и Essential представляют собой привлекательный пакет для держателей криптовалюты, которые хотят вывести безопасность своих криптоактивов на новый уровень.

Хотя на рынке доступны более дешевые устройства (Trezor One, SafePal S1, Ledger Nano S), кошельки Cobo Vault по — прежнему имеют очень разумную цену с учетом их функций.

Лучшие аппаратные кошельки до ста долларов

The benefits and challenges of POBO and COBO

Increasing international standardisation of payment formats has paved the way for more centralised processes and incentivised companies to set up payment and collection factories. Payments-on-behalf (POBO) and collections-on-behalf (COBO) are the ultimate goal of every ambitious payment and collection factory project.

Increasing international standardisation of payment formats has paved the way for more centralised processes and incentivised companies to set up payment and collection factories. Payments-on-behalf (POBO) and collections-on-behalf (COBO) are the goal of every ambitious payment and collection factory project, enabling consolidation of banking partners, high levels of transparency and maximum efficiency for financial processes. But what are the challenges, what represents best practice and how should treasury go about implementation?

The rise of common global implementation (CGI) as the international standard format for payments, actively supported by banks worldwide, has opened up new possibilities for companies to streamline their accounts payable and receivable (AP/AR) processes.

Once companies had, for example, to apply 10 different formats to connect 10 countries to their payment system, they now do so by applying one standard payment format – CGI. That said, although CGI is an internationally-recognised standard today, it does have varying individual characteristics. Nevertheless, payments and collections standardisation made possible by initiatives such as CGI worldwide and Europe’s single euro payments area (SEPA) has spurred the establishment of payment and collection factories worldwide.

When implementing POBO/COBO, questions that companies typically ask include:

• When does it make sense to set up a payment/collection factory and POBO/COBO?

• What are the greatest benefits?

• What are the challenges?

• Is a shared service centre (SSC) needed?

• How to go about implementation?

Let’s consider each of these:

When does it make sense to set up a payment/collection factory and POBO/COBO?

For POBO and COBO to deliver significant efficiency gains and a measurable return on investment (RoI), it is usually companies with subsidiaries in more than 10 countries and with a substantial annual turnover that implement centralised payment and collections hubs. Implementation projects are complex, requiring involvement by dedicated implementation teams both from the company and the bank, so significant resources and endurance are vital to bring the project to successful completion and reap the benefits.

What are the greatest benefits?

Experience suggests the most important benefits of a POBO/COBO scheme are:

• Maximum transparency: A central and real-time overview enables management at head office to track company-wide cash flows and ensure compliance.

• Reduced fraud risk: Knowing exactly where the cash is flowing helps detect and combat fraud.

• Better control of local subsidiaries: Payment/collection factories are ideal for integrating local processes and making them more visible. Monitoring local payments and providing direct feedback to local entities is an advantage of centralised and standardised processes.

• More cost-efficient payment including optimisation of payments based on value dates: With a POBO approach, companies can bundle payments according to their individual criteria and automatically select the most cost-efficient payment method and banking connection.

What are the challenges?

Inevitably with such complex projects, several challenges must be considered.

Whitepapers & Resources

Transaction Banking Survey 2019

Payments TIS Sanction Screening Survey Report

Payments Enhancing your strategic position: Digitalization in Treasury

Netting: An Immersive Guide to Global Reconciliation

Payments-on-behalf is possible for many – but not all – payment types. Tax payments, for example, must be made locally. In some countries payments-on-behalf are prohibited by law; in others such as Japan, they are highly complicated due to legal tax restrictions, so one must assess whether implementing POBO is worth the effort.

Secondly, some countries’ regulations prohibit CGI formats, while some banks still do not yet support the international format.

Apart from regulatory challenges, companies should review their internal processes. POBO and COBO support an automated cash management process, so they should not forget to integrate local payments into their cash management projection of local need for cash. It is also important to ensure that all internal receivables are correctly accounted for in the balance sheet.

The hours of operation impact on the process efficiency of payment/collection factories when they are established across continents. For example, a company has set up a payment/collection factory at its Europe head office but has subsidiaries worldwide. In that case bank statements from, say, Asia are typically available at midnight so that any (automated) cash management payments, which actually need the balances based on the actual account statement, could be initiated immediately once the bank statements are automatically processed. However, the time difference means head office employees will only start work at 7 am or later, leading to a loss of time in the processing steps.

Technology can here be used to implement global processes but with local execution. With global solutions visibility, transparency, control and management business intelligence information are all possible.

COBO presents further challenges. In order to retrieve all kinds of AR information, such as bank statements, lockbox, cheque payments or remittance advices worldwide and obtain a central overview of account balances and account activity, the statements, lockbox and other data are not only collected via the master banks of the payment factory, but usually also from local banks or AR banks, as there are no standardised formats for receivables information yet like the CGI for payments. There are four main options for circumventing this challenge:

Companies may

• Ask their master banks to collect the local bank statements lockbox and other cash management information from the AR banks. They will route all statements to the company’s collection factory. That means, however, that their master banks know all about company-wide ARs; moreover, they charge sizeable fees for this service.

• Use a Swift service bureau. Technically, only one connection is required, but the administrative component including contracts with the individual banks remains with the company.

• Set up their own Swift connections, so that all banks send their statements directly to the collection factory.

• Use specialised technology to automatically process all kinds of AR data including remittance advices that can be sent in all kinds of formats (electronic, pdf, email, paper etc.)

However, not all banks offer Swift connectivity. Individual local requirements and capabilities often result in companies using a hybrid of approaches.

For standardisation purposes, collection factories mainly use the common MT940 or camt formats for AR reconciliation. Although these formats provide considerable detail on individual items, they lack the depths that some banks provide via highly individualised reporting. These could not be mirrored in the usual and standardised set-up of a collection factory. For example, a bank in one country may deliver details, such as the number of articles or even components.

Despite the challenges, collection factories and COBO are great for providing a central, reliable overview in real time of company-wide AR. Management benefits from enhanced transparency and an exact knowledge of their local entities.

Is an SSC needed?

This is an often-asked question. The answer is fairly straightforward: an SSC landscape is not a perquisite for a payment factory, but is recommended. As mentioned earlier, payment factories across different continents face gaps in their operations due to different time zones and regional operating hours. To reap full benefit from a payment factory companies would need 24/7/365 operations. The easiest solution is to implement regional SSCs so that processes are uninterrupted. In many cases, companies run SSCs for AP/AR processes, one in each region, to support their payment and collection factory set-up.

How to go about implementation?

Successful projects require full support and buy-in from management as well as dedicated process owners to drive the project.

Prior to setting up a payment/collection factory a company should consolidate the number of banks they work with and cooperate closely with them. The aim of centralising payments and collections processes is to streamline them, with consolidation an essential component. Often, payment/collection factories use no more than five to 10 banks as master banks, depending on corporate structure. Companies thus need to individually evaluate the optimal number for achieving efficiency gains while preserving sufficient diversity: you don’t want all the eggs in one basket.

The benefit of consolidation at the outset is that less testing is required during the project, as banks are usually fairly strict about POBO and only release such payments once sufficient testing is done. As testing must be carried out for each country, payment type and bank connection one can easily imagine the work involved. So, the fewer bank connections the faster the testing.

Involving tax and legal experts with international focus is paramount for ensuring processes comply with local requirements and robust contracts with banking partners. Financial experts can help with cost-benefit analyses for each country to be included in the payment/collection factory,

The technical component needs must also be looked at, as the IT infrastructure required for a payment/collection factory is probably more comprehensive than that already established in the company. Thus, it is essential to assess the status quo and fill any gaps through additional technology.

Payment/collection factory projects are usually complex so it is important to plan sufficient time for completion, define clear milestones, measurable tasks and project responsibilities to ensure successful completion on time and to budget.

Conclusion

Various challenges must be overcome, but the reward is huge: POBO/COBO is an ideal means for providing management with enhanced control and transparency. Payment and collection factories enable company-wide standardisation and positively impact on process efficiency.

What companies particularly value about POBO/COBO – besides greater process efficiency – is improved transparency and control over company-wide cash flows. Moreover, cost reductions achieved by minimising the number of bank connects and international cash transfers as well as using domestic payments instead of foreign payments has been cited by customers as a key benefit of centralised payment and collection hubs. The extent to which companies can reduce costs naturally depends on the scope of their POBO/COBO projects, the countries they operate in, IT landscapes, workflows, bank partners and various other factors.

Due to countries’ different legal, technical or process requirements, banks and companies hybrid set-ups of payment/collection factories are most common. Evaluating all aspects, including legal and tax restrictions, internal processes, banking connections, technical capacity et al is a perquisite for a set- up that best suits the company’s needs.

Most often, POBO/COBO projects are implemented in phases starting with one region so that benefit is given before rolling it out to other regions. Establishing a POBO/COBO set-up is a far from simple project and typically takes months, or even years to complete – depending on the number of countries, currencies, legal and technical requirements et al.

Thorough planning, management buy-in and dedicated teams are thus essential for a successful project.